Press Release

Used BEV prices are stabilising according to INDICATA’s latest Market Watch report

There could be a silver lining for used BEV owners according to the latest INDICATA Market Watch report.

Average prices at the start of October were only 0.44 pp lower than at the start of September which means that used BEV prices have reduced at a slightly slower rate than other powertrains.

This marks three consecutive months without an accelerated reduction in average BEV prices, a positive sign that BEV prices are finally stabilising.

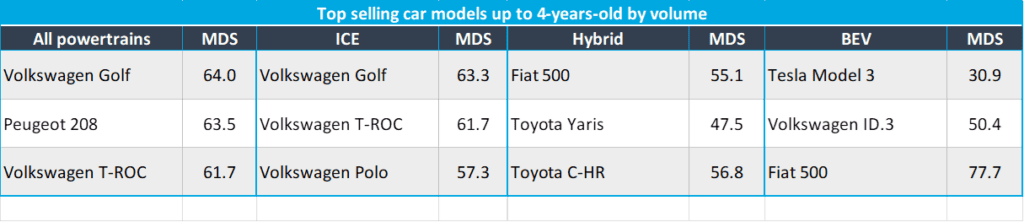

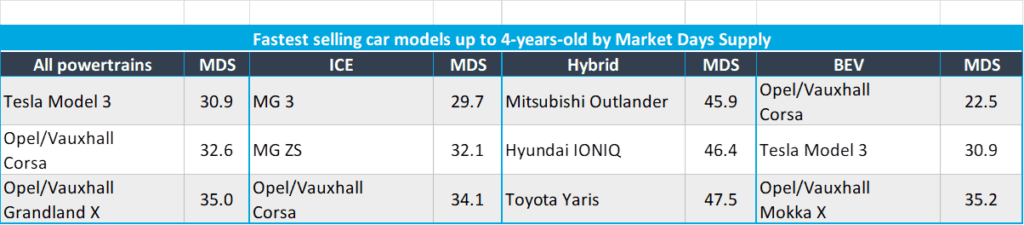

Tesla Model 3 – Europe’s top and fastest-selling EV

While used BEVs have struggled over the last year or so there are some models which are continuing to break the trend. The Tesla Model 3 is not only the top-selling BEV by volume, but also the fastest-selling model across all powertrains, with a Market Days’ Supply (MDS) of just 30.9 days.

The Opel/Vauxhall Corsa also demonstrates the importance of supply and demand with the BEV version having an MDS of just 22.5 days, making it the fastest-selling BEV powertrain. It is also performing much better than its traditional powertrain equivalent which has an MDS of 34.1 days.

Fastest-selling used cars are BEVs

Four countries out of the 13 featured in our report all saw BEVs account for the top three fastest-selling used cars during September.

| Denmark | 1 Tesla Model 3 | 2 Tesla Model Y | 3 Renault Zoe |

| Germany | 1 BMW i3 | 2 Tesla Model 3 | 3 Tesla Model Y |

| Netherlands | 1 Tesla Model 3 | 2 Tesla Model Y | 3 Cupra Born |

| UK | 1 Renault Zoe | 2 BMW i3 | 3 Hyundai IONIQ |

“After months of turmoil used BEVs could finally be settling down much to the relief of many large leasing companies, dealer groups, OEMs and banks who have suffered at the hands of falling prices over the past 12 months,” explained Andy Shields, INDICATA’s global business unit director.

“That may have all changed with used BEV prices in some countries rising in September, while others have stabilised and stopped falling. Tesla seems to remain as the aspirational used BEV brand across Europe with both the Model 3 and Model Y, while the aging but affordable BMW i3 and Renault Zoe are also both in strong demand,” he added.